Japan Equities

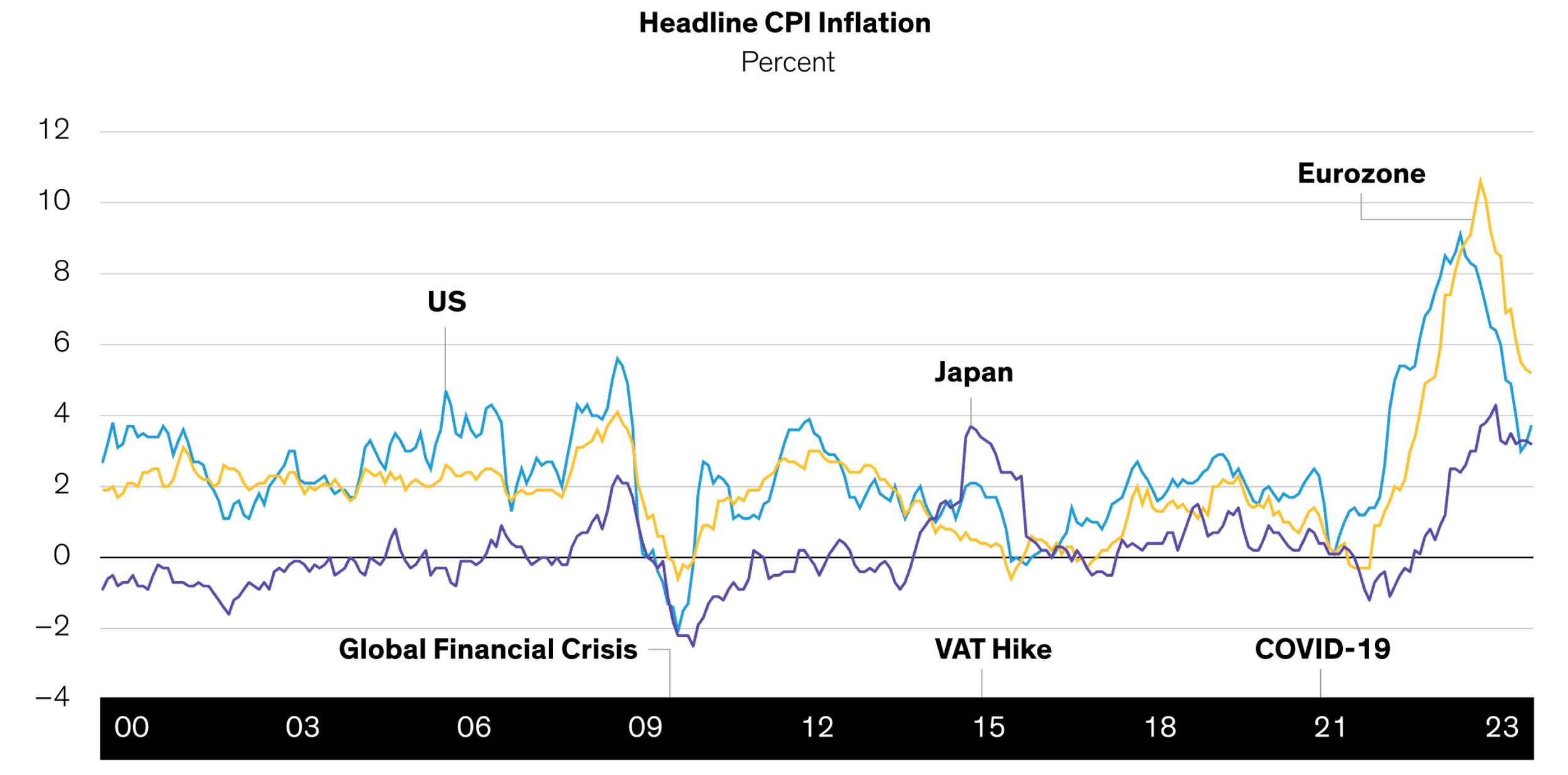

Inflation has been at the heart of the Japanese stocks’ awakening. Japan’s headline Consumer Price Index (CPI) inflation was 3.3% in July, having peaked at 4.3% earlier in the year. That’s relatively mild compared with the US and Europe, but dizzyingly high by Japanese standards (Display).

Past performance does not guarantee future results. Through July 31, 2023 Source: Eurostat, Statistics Bureau of Japan, US Bureau of Labor Statistics and AllianceBernstein (AB)

For Japanese consumers, inflation is painful, as wage increases have yet to catch up with the rising cost of living. Inflation also raises procurement costs for businesses and leads to tighter monetary policy and higher borrowing costs. However, pushing the Japanese economy out of the flat-price, zero-interest comfort zone may be exactly why profound changes are taking place.

Companies that have long been reluctant to raise prices for fear of being undercut by competitors are no longer absorbing rising costs by squeezing their own profit margins. Instead, they are passing on higher prices to customers. This started with companies more exposed to imported materials, such as paper mills and steelmakers, which helped support higher stock prices. Now, even domestically oriented industries are doing the same, causing the CPI to catch up with producer price inflation.

Workers are unlikely to remain content with the miniscule wage increases they have endured for decades, particularly as the working-age population is shrinking. At some point, we anticipate real wages to turn positive, resulting in more spending power.

Consumers are also likely to move their savings from bank deposits, which pay virtually no interest, to higher-yielding assets. According to the Bank of Japan (BOJ), Japanese households held some 2,043 trillion yen of financial assets as of the end of March, 54% of which were in bank deposits and just 11% in equities. Even a small change in those percentages can translate into huge stock market inflows; a major expansion of Japan’s individual saving account scheme, nicknamed NISA, in 2024 makes this a distinct possibility.

Faced with a shrinking labor force, potentially higher wages and a higher cost of capital, corporations must boost productivity. This, in our view, is creating opportunities in industries such as IT services and human resource services.

Corporations must also do something with their cash piles. Companies representing 53.5% of Japan’s market capitalization had a net cash position on their balance sheets at the end of 2022, compared with 39.4% in the US and 22.8% in the eurozone (Display). Dividend payouts and stock buybacks, which both return cash to shareholders, had already been increasing over the past decade, but—more importantly—we believe that inflation will make it easier for management to find ways to better reinvest cash to grow their businesses. And after several rounds of reform starting with the 2014 Stewardship Code, corporate governance has improved, and managements are taking a more disciplined approach to capital deployment.

Improving profitability could draw attention to overlooked globally competitive companies. For instance, while Japan no longer has world-leading chipmakers, it still has numerous indispensable players in the global semiconductor supply chain, such as silicon wafer producers and production equipment makers.

Many Japanese materials and component makers are key enablers of the global green-energy industry. There are also world-leading factory automation companies supporting global manufacturers, as well as companies with attractive intellectual property, such as video game and toy characters.

Even banks look more appealing than a few years ago, as higher interest rates push up net interest income. And a post-pandemic recovery in tourism is helping to boost sales at many consumer companies, such as cosmetics makers and shopping outlets.

Since the “bubble economy” burst in 1990, the Japanese equity market has seen numerous false dawns. Today, we believe that ongoing inflation can act as an antidote for long-entrenched deflationary behaviors that have held back the market.

To be sure, if Japan’s inflation gets out of hand, the BOJ may be forced into a steep rate-hike cycle a la the US Federal Reserve and the European Central Bank. That could cause quite a shock wave, given Japan’s huge government debt mountain. But, so far, the BOJ appears to expect inflation to settle down next year and beyond, to manageable levels. With global inflation likely to remain relatively high for some time, central banks in many countries are likely to maintain a hawkish stance. In this environment, we believe that Japanese equities offer a unique market where the ripple effects of inflation may deliver outsize benefits to a broad group of companies and support a sustained recovery for investors.

Other News